Wirestock Creators // Shutterstock

Our dogs might not play “Creep” by Radiohead while baking and then subsequently eat an entire boxed cake recipe when they’re lonely, but that doesn’t mean they don’t feel it. Like all of us, dogs require a certain level of socialization — both with their own kind and with their humans. And when those needs go unmet, they can start feeling agitated and, to borrow a label from Thom Yorke, act like total weirdos.

Loneliness, as we understand it, is a bit of a human concept; dogs who don’t enjoy enough social time don’t sit down on the couch, sigh, and think to themselves, “I’m really lonely.” Still, just like with people, isolation can leave our pups in a particular kind of distress. From the outside, our dogs’ expressions of that grief might seem strange or even frustrating, but in reality, separation anxiety and other behaviors associated with canine loneliness come from a place of real pain.

If you suspect your dog is feeling neglected or understimulated, it’s worth taking seriously. But try to fact-check your suspicions. Dr. Ori Stollar, a veterinarian and behavior specialist with Massachusetts Veterinary Behavior Service, has been approached by many clients who assumed their dog had separation anxiety because they heard them barking whenever they left home and returned. “Then, they took my advice and recorded the dog alone and found out that once they were gone, the dog spent most of the time sleeping,” he says, “which is normal.”

So how can you tell if your dog is actually lonely? Kinship shares some expert advice.

How can you tell if your dog is lonely?

Your dog might not tell you they’re feeling lonely, but there will be signs. Dr. Stollar says that different dogs have different needs and coping mechanisms, just like humans do. “Some people don’t mind being alone or might show subtle signs when lonely,” he says, “and so do dogs.”

If you suspect your dog is feeling isolated, Dr. Stefanie Schwartz, a board-certified veterinary behaviorist and founder of Civilized Pet, recommends looking for agitated behavior. Agitation doesn’t necessarily mean your dog is lonely, but it’s a good starting point to determine if something might be wrong.

Signs your dog might be lonely (or has some other unmet need) can include:

Destructive behavior

Think “ripping through the closet and grabbing shoes,” Dr. Schwartz says. Sometimes, this can escalate into agitation and even more mayhem.

Restlessness

If your dog seems to be wearing a track into the floor, that’s a sign they can’t settle.

“It could be lying down for a second, getting up and walking to the window and pacing along the windows, and going back to bed for two minutes and getting up again,” Dr. Schwartz says. “Or it could be nonstop wandering around the house, and that can escalate to running.”

Ursula Page // Shutterstock

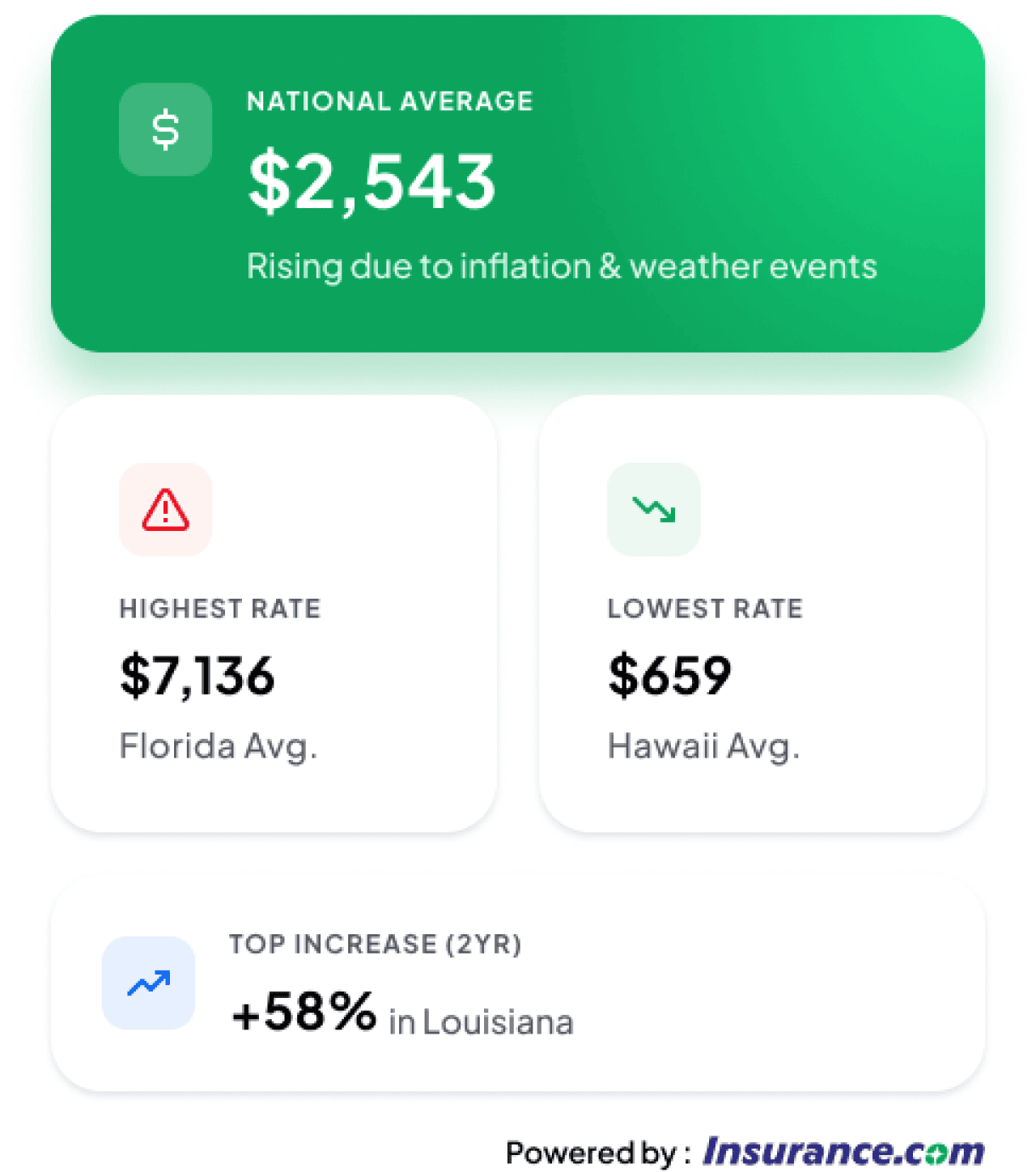

Rate increases over the past few years have been hitting homeowners hard, thanks to increasingly volatile weather, inflation, and other factors. 2026 should see stabilization in the home insurance market, but, depending on where you live, you probably shouldn’t count on seeing lower rates on your renewal.

The Consumer Federation of America’s April 2025 report, Overburdened, found that U.S. homeowners spent $21 billion more on homeowners insurance in 2024 than in 2021.

Although the market in general is improving, with AM Best elevating the market segment from negative to stable in December 2025, it may be a while before many homeowners see any sign of lower rates.

What’s driving home insurance rate increases? Will rates go down in 2026, or ever? What can homeowners expect when it comes to their insurance coverage and bills, and how do they feel about it? While we see improvements on the horizon, home insurance remains a source of sticker shock and frustration. Read on for insights from Insurance.com, data, and details on the state of home insurance in 2026.

Insurance.com

Home insurance rates rise: Here’s what’s to blame

Home insurance rates have been climbing over the past few years, with homeowners facing sticker shock both on renewal and when shopping for new coverage. There are several reasons, some less obvious than others.

- Severe weather and natural disasters. 2025 began with some of the worst wildfires in history, with billions of dollars in damage resulting from the Palisades and Eaton fires in California. Following several years of devastating wildfires and hurricanes, along with increasing damage from storms nationwide, home insurance companies responded with rate increase requests. The good news? A quiet Atlantic hurricane season provided some breathing room.

- Increased construction costs. Inflation has made all the materials used to build and repair houses more expensive. The more it costs to rebuild a home, the higher claim costs become, and insurance companies respond by increasing premiums to offset the additional expenses.

- Litigation. High numbers of lawsuits, particularly in states where the law has been favorable toward those suing insurance companies, drive up costs for insurance companies, which are again passed on to consumers.

- State regulations. Some states have much str

aniqpixel // Shutterstock

Back in 2016, cold email was simple. “You could plug in a brand new account on a brand new domain, and on day one, send a hundred to 300 emails — absolutely zero problem,” recalls Benny Rubin, CEO of email deliverability specialists Senders..

But things have changed dramatically. “Mailbox providers have really clamped down on cold email because of the sheer volume,” he explains.

After nearly a decade helping companies navigate these changes, Rubin shares insights with Apollo.io on key mistakes that consistently hurt cold email campaigns.

Mistake #1: Using open rates to measure campaign success

Open rates are a go-to metric for measuring email performance, but they’re increasingly unreliable.

When security systems scan emails within fractions of a second, bot opens happen, artificially inflating your numbers. Privacy features block tracking pixels, deflating them. Email client updates can swing your rates dramatically overnight.

Many sales teams make critical campaign decisions based on open rate fluctuations that might just be technical noise. Even worse, focusing on open rates can lead to optimizing the wrong things, like flashy subject lines that get opens but don’t generate business results.

The fix: Focus on reply rates, especially interested replies, as your primary health metric. These represent actual human engagement and correlate directly with revenue. Use open rates as a secondary indicator, and look for dramatic changes over time rather than absolute numbers.

Mistake #2: Skipping the domain aging process

New domains are like strangers on the internet. They have no reputation, good or bad. Email providers are suspicious of domains that suddenly start sending hundreds of emails with no history.

There’s something called a “fresh domain blacklist” that can affect domains for up to 90 days after purchase. This is why advice you see to buy dozens of domains and rotate through them is a hack, not a sustainable strategy.

The fix: Purchase domains well in advance (at least 90 days before use) and warm them up properly. For immediate capacity, use subdomains of existing aged domains. Then make sure you’re setting up your SPF, DKIM, and DMARC authentication.

Mistake #3: Hiding or removing unsubscribe links

Some sales teams remove all links, including unsubscribe options, after hearing that “links hurt deliverability.” This backfires because unsubscribe links signal responsible behavior to email providers like Google.

The bigger threat is spam complaints. When people can’t easily unsubscribe, they’re more likely to mark you as spam, which is far more damaging to deliverability than including an unsubscribe link.

The fix:

BritCats Studio // Shutterstock

In today’s fast-moving digital economy, growth depends on strong, trusted relationships with vendors, suppliers, and partners. These third parties are often essential to modern business operations; however, they also open the door to a range of risks, from regulatory fines to operational slowdowns. Many organizations have already felt the impact of these risks becoming reality firsthand.

The State of Trust Report by Vanta, which surveyed over 3,500 IT and business leaders in the U.S., U.K., and Australia in July 2025, found that nearly half (46%) of all respondents experienced a data breach from a vendor after beginning their partnership.

This data makes it clear that vendor risk doesn’t end at onboarding and reinforces the need for continuous oversight through a strong third-party risk management (TPRM) program. A TPRM program will operationalize your approach to identifying, assessing, and managing the risks associated with all external vendors, suppliers, and partners that have access to your organization’s operations.

While often used interchangeably, vendor risk management (VRM) focuses specifically on a subset of third-party risks. A truly effective TPRM strategy extends beyond vendor contracts to manage risks across the full spectrum of third-party relationships—including suppliers, partners, and service providers. This means addressing multiple risk types, from cybersecurity and privacy to ESG, legal, and any reputational risks.

This guide will review the common challenges of TPRM strategies, explore how teams are working to close those gaps, and highlight why AI and automation are crucial for scaling TPRM efforts.

Key takeaways

- While often used interchangeably, VRM is a subset of TPRM focusing on the security and compliance risks associated with vendor relationships. TPRM is the practice of identifying, assessing, and managing all types of risk across all external partners.

- Many best practice TPRM frameworks address the full range of third-party risk exposure.

- Nearly half (46%) of IT and business leaders say that one of their vendors experienced a data breach since they started working together, highlighting the need for continuous TPRM.

- Mature TPRM programs offer significant benefits, including enhanced security, improved compliance, greater operational resilience, and stronger vendor relationships.

- Organizations that effectively manage third-party threats prioritize their vendor portfolio criticality and implement structured, risk-based reassessment schedules. This programm